Money Movement: How Funds Are Transferred Through Payment Systems

Money movement refers to the structured process through which funds are transferred between parties across financial networks. It is not a single action, but a coordinated sequence involving instruction, validation, routing, clearing, and settlement across multiple institutions.

Although payments appear instantaneous to users, the underlying system spans several layers of infrastructure, each performing a specific function.

Modern financial technology has increasingly abstracted this complexity through software-based interfaces, while parallel systems focus on preventing fraud and ensuring transactional integrity as funds travel through digital channels.

What Money Movement Involves

The transfer of value between a payer and a recipient, known as money movement, takes place through interconnected payment rails in a structured end-to-end process designed to ensure accuracy, consistency, and finality.

At a high level, the process includes:

Initiation and authorisation

Routing through payment networks

Clearing between financial institutions

Settlement of funds

Post-transaction reconciliation

These stages are executed by different entities, yet must remain synchronised to maintain trust and operational stability.

How it Works?

Below is a breakdown of the key steps involved in money movement from initiation to final settlement.

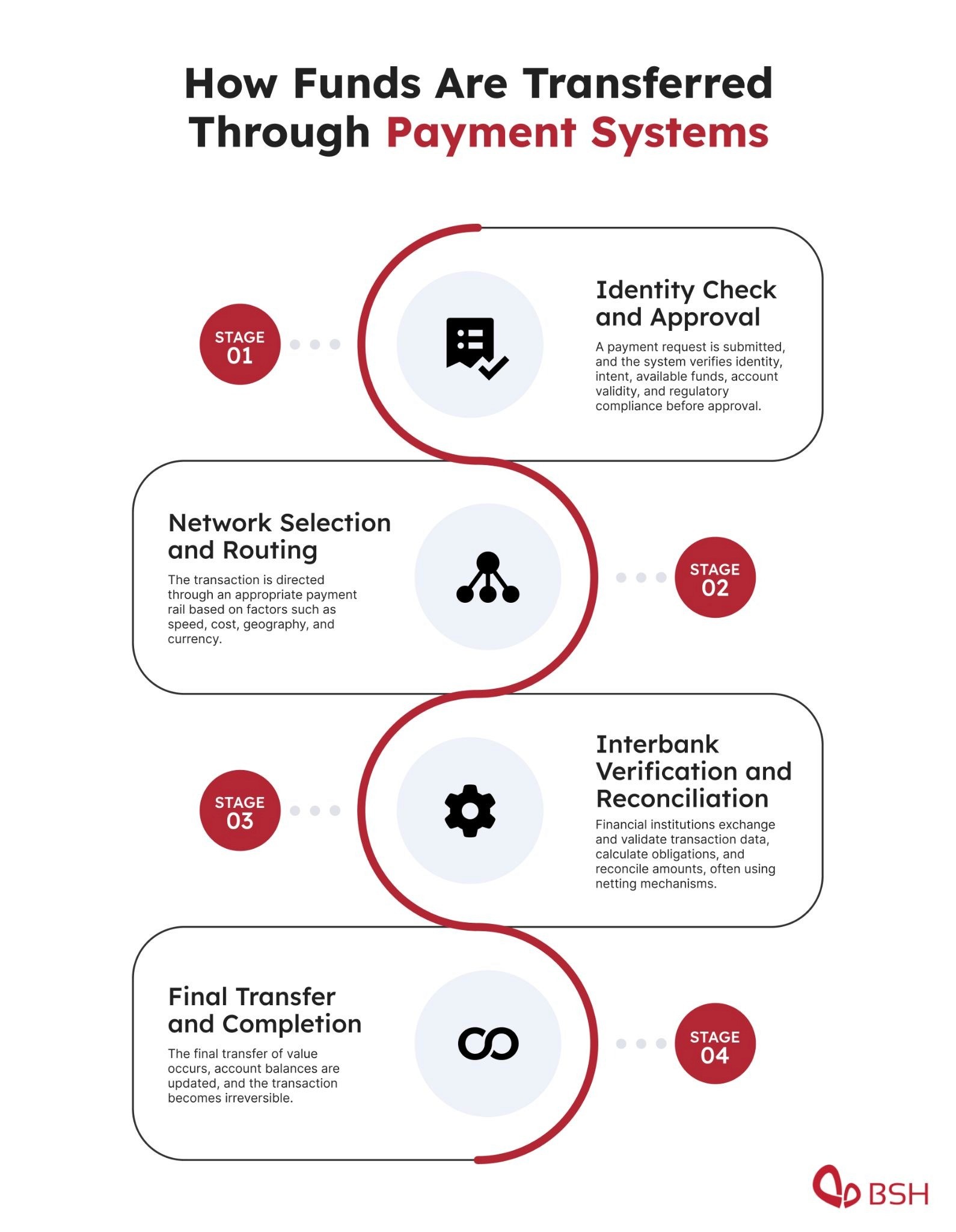

Stage 1: Initiation and Authorisation

The process begins when a payer submits a payment instruction. This step verifies intent and confirms identity through authentication methods such as passcodes, biometrics, or secure credentials.

At this stage, systems also evaluate:

Availability of sufficient funds

Validity of account details

Compliance with regulatory requirements

Only after these checks are satisfied is the transaction approved for further processing.

Stage 2: Routing Through Payment Networks

Once authorised, the transaction is directed through an appropriate payment rail. The choice of route depends on factors such as geography, currency, speed requirements, and cost.

Common categories of payment networks include:

Domestic bank transfer systems

Card-based networks

Real-time payment infrastructures

Cross-border correspondent banking arrangements

Each network has distinct operational characteristics. Some prioritise immediacy, while others optimise for cost efficiency or broad geographic coverage.

Stage 3: Clearing Between Institutions

Clearing is the stage where financial institutions exchange and validate transaction data. Obligations between sending and receiving institutions are calculated, often through netting arrangements that reduce the total number of settlements required.

Depending on the system, clearing may occur:

In batches at scheduled intervals

Continuously in real time

This stage ensures that both parties agree on transaction details before funds are transferred, reducing the likelihood of disputes or inconsistencies.

Stage 4: Settlement of Funds

Settlement represents the final transfer of value between financial institutions. At this point, ledger balances are updated, and the transaction becomes final and irrevocable.

Settlement models vary:

Deferred settlement: transactions are processed in batches, often introducing delays

Real-time settlement: funds are transferred immediately between institutions

Cross-border settlement introduces additional complexity due to currency conversion, intermediary institutions, and enhanced compliance checks.

Payment Infrastructure Types

Each payment system is built to serve a specific purpose, prioritising factors such as speed, cost, scalability, or geographic reach. Below are the different types of payment systems used in money movement.

Bank Transfer Systems

These systems are commonly used for salaries, supplier payments, and recurring transactions. They are cost-effective but typically slower due to batch processing.

Card-Based Systems

Card networks allow immediate authorisation at the point of transaction. However, final settlement between institutions usually occurs later.

Real-Time Payment Systems

These infrastructures enable near-instant transfer of funds between participating institutions, improving liquidity and reducing processing delays.

Cross-Border Systems

International transfers rely on intermediary institutions to route funds and convert currencies, introducing additional time and cost.

Digital Wallet Systems

Wallet-based systems abstract underlying payment rails by allowing users to store and transfer value within a unified interface.

Fraud Risk and Compliance Controls

As payment systems become faster and more accessible, exposure to financial crime increases. Common threats include account misuse, identity manipulation, and unauthorised transaction attempts.

To mitigate these risks, systems apply real-time monitoring techniques that assess behavioural patterns, device information, and transaction history. These signals help determine whether a payment should proceed, be flagged, or be blocked.

In parallel, regulatory frameworks impose mandatory controls, including:

Identity verification requirements

Anti-money laundering monitoring

Sanctions screening obligations

These safeguards introduce additional processing steps but are essential for maintaining system integrity and legal compliance.

Digital Transformation of Money Movement

Traditional financial infrastructure has evolved into programmable systems that allow payments to be initiated and managed through software interfaces.

This shift enables:

Automated payment execution

Dynamic selection of payment routes

Real-time transaction visibility

Integration of payments into non-financial platforms

As a result, money movement has become more embedded within digital products rather than operating solely through traditional banking channels.

Key Benefits

Operational autonomy: Teams can manage and trigger payments without manual banking processes

Faster execution cycles: Reduced dependency on batch-based or manual approvals

Improved decision-making: Real-time visibility supports better financial control

Reduced operational workload: Automation limits repetitive payment processing tasks

Scalable workflows: Systems can handle growing transaction volumes without proportional staffing increases

Operational Challenges

Despite significant advancements, several structural limitations remain.

System Fragmentation

Different regions operate distinct payment infrastructures, limiting global interoperability.

Legacy Processing Models

Some systems still rely on batch-based processing, reducing speed and efficiency.

Transaction Errors

Incorrect account details, network failures, or incomplete data can lead to delays or failed transfers.

Liquidity Management

Financial institutions must maintain sufficient funds across multiple accounts and jurisdictions, particularly when processing high transaction volumes.

Key Takeaways

Money movement is a foundational component of the global financial system, enabling the transfer of value across individuals, businesses, and borders. While it appears simple at the user level, it relies on a complex sequence of validation, routing, clearing, and settlement across interconnected networks.

Ongoing improvements in infrastructure have increased speed, automation, and accessibility. However, these gains also require stronger fraud controls and stricter compliance oversight. The overall system continues to evolve towards greater efficiency, while maintaining the balance between speed, security, and regulatory responsibility.

Frequently asked questions

Why don’t all payment systems use the same process for transferring funds?

Different systems are designed for different priorities, such as speed, cost efficiency, geographic coverage, and regulatory requirements. As a result, each payment rail follows a distinct operational model rather than a universal standard.

What determines whether a transaction is processed instantly or in batches?

Processing speed depends on the underlying infrastructure. Real-time systems are designed for immediate processing, while traditional systems group transactions into batches to optimise cost, liquidity, and operational efficiency.

How do financial systems ensure data accuracy during transfers?

Accuracy is maintained through multiple validation layers, including message matching between institutions, automated error detection, and reconciliation processes that compare records before final confirmation.

What role do intermediaries play in international payments?

In cross-border transactions, intermediaries help connect financial institutions that do not share direct relationships. They assist with routing, currency conversion, and compliance checks across jurisdictions.

Why is visibility into payment status important for businesses?

Real-time visibility helps organisations manage cash flow, reduce operational uncertainty, and detect issues early in the payment lifecycle. It also supports better financial planning and decision-making.